Flood Risk 2.0

Flood Risk 2.0 is upon us and unfortunately for many homeowners, the outlook is grim. In 1968, the Federal Emergency Management Agency (FEMA) administered flood insurance through the National Flood Insurance Program (NFIP). Since then, FEMA has written flood insurance on a rate table based on the flood zone and the elevation difference of a property within a flood zone.

When we refer to flood zones, there are essentially two classes of flood zones being a high hazard flood zone and a low to moderate risk flood zone. A high hazard flood zone begins with the letter A or V and typically ends in E, forming an AE flood zone. A low to moderate hazard flood zone is classified as the letters B, C, or X. For a homeowner that has a mortgage that is backed by a bank insured by the FDIC, they are required to carry flood insurance if the structure is located in the A or V flood zone.

Within a flood zone designation, homes are classified as Pre-FIRM or Post-FIRM. FIRM indicates Flood Insurance Rate Map. The FIRM is essentially the date that the municipality began enforcing flood mapping within construction planning which is why you see some older homes that are considered a slab-on-grade type foundation, and newer construction that is built up higher within the same community.

From 1968 through 2003, FEMA essentially ran the NFIP flood program at a break-even. In some years they would pay out more claims than dollars that they took in, but the following year they would wash out those claims. However, in 2004 and 2005 FEMA took on shock losses to the program that caused the program to become massively unprofitable. The biggest shock loss event was Hurricane Katrina with claims over $16,000,000,000 followed by Hurricane Ike in 2008 at over $2,600,000,000, Hurricane Irene at over $1,100,000,000, and Hurricane Sandy at over $10,000,000,000. The compounding of these storms created the program to be in over $24,000,000,000 of debt prior to Sandy hitting which then increased the debt even further.

As a result, on July 6, 2012, Congress voted to enact the Biggert-Waters Act. Most of us learned about Biggert-Waters on October 1, 2013, when it caused flood insurance rates to go from $2,000 to $10,000 overnight for slab-on-grade-type properties. The massive overnight rate increases were later revised with the Homeowner Flood Insurance Affordability Act of 201, which put annual caps on rate increases for primary residences at 18% per year. Another part of the Biggert-Waters Act that is coming to light on October 1, 2021, is the line item for “Establishing a technical mapping advisory council to deal with map modernization issues.” This line has become considered Risk Rating 2.0.

In 2012 FEMA started developing Risk Rating 2.0 and it essentially transforms the rating of flood insurance for the first time since 1968. From 1968 through October 1, 2021, flood insurance was rated on flood zone and the (+) or (-) base flood elevation difference. For example, if a house is built to a 10-foot base flood elevation and the first living floor of the house is 12 feet, the house is rated as a +2 elevation. That has since totally changed with Risk Rating 2.0

The other change with Risk Rating 2.0 is the removal of grandfathering overtime for policies. FEMA has always honored that if a house was built to a certain flood zone and base flood elevation for the life of the policy, a homeowner can rate themselves to that map. For example, if a house was built in 1980 at an 8-foot base flood elevation and in 2003 the map changed to a 10-foot base flood elevation making a house “out of compliance” FEMA allowed a home to be rated as “built-in compliance” and grandfather their flood insurance rate. This provision has been critical to protecting homeowners living in flood zones.

With Risk Rating 2.0 it removes grandfathering and many other policyholder provisions with an 18% annual rate increase every year until it is removed. While 18% is a lot, it becomes even more when you compound 18% annually across 10 years. Using the example of a $1,200 premium rate –

|

Year |

Premium |

|

2021 |

$1,200 |

|

2022 |

$1,416 |

|

2023 |

$1,670 |

|

2024 |

$1,971 |

|

2025 |

$2,326 |

|

2026 |

$2,745 |

|

2027 |

$3,239 |

|

2028 |

$3,822 |

|

2029 |

$4,510 |

|

2030 |

$5,322 |

At the end of 10 years that rate has increased to $5,322.

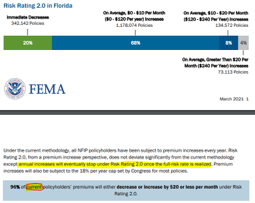

An important consideration in explaining Risk Rating 2.0 is that not all homes are affected with an increase. We are seeing about 20% of homes in Florida affected with a rate decrease.

With Risk Rating 2.0 it does not consider homes in flood zone within the core rating elements. Each risk is individually calculated on a proprietary formula to FEMA based on: different types of flood event risk, the distance to the coast, and the cost to rebuild the home.

Homes that are within the proximity of tidal water (Gulf/Ocean, Canal, Lake or Other) and higher value, regardless of the location, are going to be affected by massive rate increases. The challenge of rating the risk to the value of rebuilding the house is that the flood policy caps its coverage at $250,000. NFIP is now charging a higher rate for a 5,000 square foot home with $250,000 of coverage compared to a 2,000 square foot home with $250,000 of coverage.

A common question that we have received is, why nobody knew about the rate increases. Unfortunately, rate increases for new policies take effect on October 1, 2021. While FEMA released access to their Rating 2.0 rates for insurance agents on August 30, 2021, to effectively give a 30 days’ notice of new rates. However, renewal policies will have a bit more time to adjust with the Rating 2.0 system taking effect next spring on April 1, 2022.

The second challenge is that FEMA published documentation in March 2021 that only 4% of “current” policyholders in Florida will see a rate increase over $240 per year. In our professional opinion, they falsely represented rate increases to avoid public backlash by using the phrase “current policyholders”. In the example above of a $1,200 premium increasing by 18%, it is a $216 rate increase, so it is less than $240 per year on FEMA’s published chart.

From an actual rate example standpoint, we are seeing the following happen on risks within the NFIP

- 63rd St and 30th Ave N, St. Petersburg, FL 33710

-

HomeValue – $350,000

HomeValue – $350,000- Foundation – Slab on Grade

- NFIP Risk Rating 1.0 – $3,663

- NFIP Risk Rating 2.0 – $1,755

- Private Flood – $446.26

- E Vina Del Mar Blvd, St Pete Beach, FL 33706

-

Home Value – $1,500,000

Home Value – $1,500,000- Foundation – Elevated on Enclosure

- NFIP Risk Rating 1.0 – $636

- NFIP Risk Rating 2.0 – $11,628

- Private Flood – $1,942.50

3. FeatherSound, Clearwater, FL 33762

-

Home Value – $450,000

Home Value – $450,000- Foundation – Slab on Grade

- NFIP Risk Rating 1.0 – $1,658

- NFIP Risk Rating 2.0 – $3,450

- Private Flood – $4,465.65

4.Symphony Isles, Apollo Beach, FL 33572

-

- Home Value – $995,000

- Foundation – Slab on Grade

- NFIP Risk Rating 1.0 – $824

- NFIP Risk Rating 2.0 – $10,578

- Private Flood – $2,508.45

5. Seminole Lakes, Seminole, FL 33777

-

- Home Value – $400,000

- Foundation – Slab on Grade

- NFIP Risk Rating 1.0 – $3,663

- NFIP Risk Rating 2.0 – $3,877

- Private Flood – $1,622

6.Vina Del Mar, St Pete Beach, FL 33706

-

- Home Value – $700,000

- Foundation – Elevated Slab on Fill

- NFIP Risk Rating 1.0 – $1,658

- NFIP Risk Rating 2.0 – $8,508

- Private Flood – $2,707

One other common question that we are receiving is about doing an assumption on a current policy. Most policies are able to be assumed, however, keep in the 18% rate factor still applies to assumed policies.

The long and short of these changes is that unfortunately, FEMA did not fully disclose what is changing. For much lower elevation, coastal, and higher value homes, you are going to see huge rate increases. There are private market solutions that still come in significantly less than FEMA. However, they are increased compared to the current rates that we have been accustomed to seeing since 1968. Property owners need to be prepared as to what this means for their home and the value of the home as this is a massive change and the biggest change in the history of FEMA. The Biggert-Waters Act only affects slab on grade homes or below elevation homes. With this change, we are seeing a vast majority of coastal (we live in Florida and most flood zones are coastal) and high-value homes hit with massive rate increases.

About Jake Holehouse:

Jake Holehouse is the President of HH Insurance in St. Petersburg, FL. Jake is the flood insurance advocate appointed by the City of St. Petersburg City Council; Pinellas County Commission; St. Pete Beach Commission and other local municipalities. He is considered the leading flood expert across Florida in understanding FEMA issues and how it correlates to the private market and real estate. He founded HH Insurance with his father, Ron Holehouse, in June 2018 and they have experienced rapid growth since the agency has opened. Jake grew up in the insurance industry working for his father’s agency during high school, at Holehouse Insurance in St. Petersburg, FL. After graduating from Florida State University, Jake worked for American Strategic Insurance (ASI) as a national account manager, specializing in the national home builder accounts. Following ASI, he decided to work alongside his father again at Holehouse Insurance. They grew the business at an astronomical rate, eventually selling the agency to Regions Insurance, an affiliate of Regions Financial Corporation. Following Regions Insurance, Jake worked at Heritage Insurance Holdings as an Executive Vice President of Business Development and assisted in product expansion from 3 states to 13 states. Seeing the opportunity of opening a new independent agency, Jake opened HH Insurance in June 2018. During Jake’s time at Florida State University, he earned his Bachelor’s and Master’s degree in Risk Management and Insurance. Additionally, he also earned a Chartered Property Casualty Underwriter (CPCU) designation. Jake sits as an advisor to the risk management and insurance program at Florida State University, as well as multiple local community service positions.

**This blog provides a brief overview of the terms and phrases used within the insurance industry. These definitions are not applicable in all states or for all insurance and financial products. This is not an insurance contract. Other terms, conditions and exclusions apply. Please read your official policy for full details about coverage. These definitions do not alter or modify the terms of any insurance contract.